Shifting Paradigms: Currency Risk and Opportunity in a Fractured World

03/07/2026

The global currency backdrop is being reshaped by persistent external imbalances, rising geopolitical friction, and a move away from the integrated trade and capital regime that defined the past three decades. While the US dollar remains dominant, its position looks more contested as reserve managers diversify, supply chains fragment, and scrutiny of the US external position intensifies. Our central conclusion is that a more fractured and multipolar world should create both greater currency risk and a broader opportunity set for investors, strengthening the case for a more active and diversified approach to currency management.

From Globalisation to Fragmentation

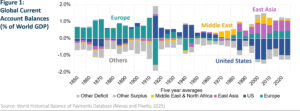

Global trade and financial imbalances are elevated by historical standards, with current account imbalances exceeding levels seen in the mid 19th century when imperial Europe dominated global trade and enjoyed substantial investment income from its overseas assets. Today, surpluses in East Asia and Europe together exceed those earlier surpluses as a share of global GDP. Unlike in previous eras the United States has, over the past 25 years, borne nearly the entire corresponding global deficit [Figure 1]. In doing so, it has so far defied the “Triffin dilemma” which posits that the persistent trade deficits involved in issuing global reserve liabilities eventually erode confidence in the currency.

In the US, these persistent deficits are increasingly viewed by some as evidence that the current global system exists at the detriment of the US. While this interpretation is not entirely accurate, it helps to explain today’s backdrop of rising tensions and shifts in trade policy. The result has been a move away from multilateralism toward a mercantilist stance, and in some cases more assertive quasi imperial behaviour towards regional neighbours such as Venezuela and Cuba. More broadly, the core logic has shifted from system stability and mutual gains from trade to a more transactional, zero-sum framework.

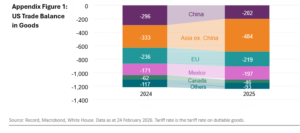

When judged by its centerpiece tariff policy, mercantilism has not delivered the intended results. Tariffs have risen to levels last seen in the early 20th century under President Mckinley, yet the impact on the trade balance has been limited. The government collected $260bn in tariff revenue in 2025, but the goods trade deficit remained broadly unchanged from its pre-tariff level in 2024 [Appendix Figure 1]. Instead, the deficit has been redistributed to other parts of Asia as exports are rerouted via third countries. First year Economics undergraduates would be able to tell you why it’s not working; the current account is the difference between gross saving and investment. Tariffs have boosted government savings, but their effect is nullified when that revenue flows out via lax fiscal policy.

As a result, these global imbalances persist, reinforcing a broader shift to a more multipolar world order. China last year posted a record trade surplus and since the early 2000s has more than tripled its share of world income, largely at the expense of Europe and parts of Asia. At the current trajectory, China’s growth and rising share of global output suggest that it will stand alongside the US as a competing hegemon by the end of the decade. In this evolving landscape, the EU finds itself stranded, and needs to cultivate new economic partnerships with similarly marginalised economies to form a more cohesive “middle bloc,” echoing the framework outlined by Mark Carney in his Davos remarks [Figure 2].

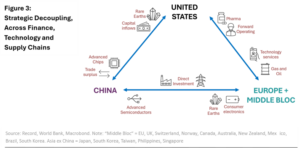

Within this emerging multipolar system, a web of strategic interdependencies has developed, helping to anchor stability by raising the cost of disruption. Yet, decoupling is well underway [Figure 3]. In global finance, reserve managers are attempting to diversify away from overreliance on the US dollar – most visibly through increased allocations to gold – while geopolitical tensions, including the Iran conflict, have revived discussion around non-dollar trade in commodities. In energy, both Europe and China are accelerating the transition toward renewables to reduce dependence on Russian and Middle Eastern supplies. In technology, meanwhile, the US and China continue to exert leverage through critical inputs such as semiconductors and rare earths, but both are working to localise supply chains and mitigate these dependencies.

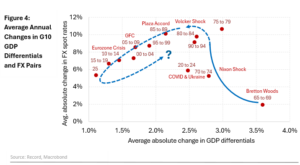

It follows that continued economic decoupling is likely to increase dispersion across economies and raise the frequency of supply side disruptions. Historical experience offers some guidance for the implications for FX markets. In the 1960s, dispersion was pronounced but currency volatility remained contained under the Bretton Woods system. Following the Nixon shock in the 1970s and the transition to floating exchange rates in the 1980s, a decline in economic dispersion during the era of hyper globalisation led to a steady compression in currency volatility. If supply shocks are more prevalent and the global response less synchronised, it implies that – absent heavy FX management – currency volatility will trend structurally higher [Figure 4].

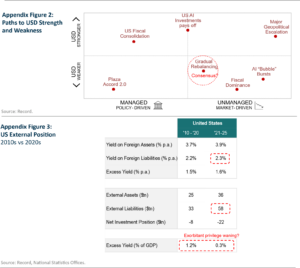

Despite these structural shifts, currency markets have remained relatively stable. However, strong US asset and currency returns have pulled global investors into outsized dollar exposures, leaving many uncertain about the outlook. Plausible paths diverge; dollar weakness could be managed – via a coordinated depreciation akin to the Plaza Accord, though requiring quixotic alignment across China, Europe, and Japan – or unmanaged, driven by fiscal dominance or a systemic shock, for example emanating from the AI sector. Conversely, dollar strength could reassert itself through renewed policy discipline after the mid-term elections, further geopolitical escalation in the absence of alternative safe havens, or if AI-related investments prove transformative and translate into sustained tradeable productivity gains [Appendix Figure 2].

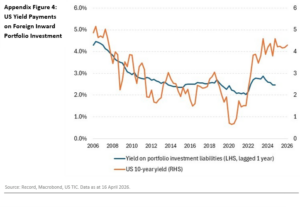

The sustainability of the US external position increasingly sits at the heart of these scenarios. The US has long benefited from an “exorbitant privilege” – the ability to borrow cheaply while earning a premium on its overseas investments – which generated around 1.2% of GDP in net investment income over the previous decade and helped to offset trade deficits. This buffer is now eroding. As US foreign liabilities have expanded from $31tn in 2015 to $58tn in 2025, the income advantage has been largely extinguished, despite still favourable financing conditions for the US and an unchanged yield gap of about 2% p.a. between foreign assets and liabilities [Appendix Figures 3 and 4].

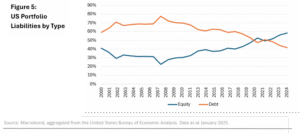

A key offset to rising Treasury yields has been a tectonic shift in how the US funds itself, with foreign financing rotating away from treasuries towards equity market investment [Figure 5]. This could help to explain the US dollar’s resilience to a worsening fiscal outlook, but conversely introduces a new axis of risk in continued confidence in US corporate earnings and technology leadership. Moreover, as these flows are inherently pro-cyclical, they may over time encourage foreign investors to raise strategic hedge ratios if greater co-movement with the dollar emerges over longer time horizons and across frequencies.

The implication is that the sustainability of the US dollar now hinges on a handful of variables: whether fiscal policy moves toward consolidation or tips into fiscal dominance; whether the AI investment cycle delivers durable productivity gains or unwinds as a misallocation of capital; and how geopolitical relationships evolve with key allies and funding partners – particularly Europe, Canada, and Japan – in both Treasury and Equity markets. Investors appear skewed toward the more pessimistic side of this distribution, but options markets imply a near-term premium for the dollar as energy shock insurance.

Emerging Investor Themes

Our discussions with investors on these topics point to several emerging themes:

- There is increased scrutiny of the US dollar’s diversification properties, which may prove more variable given the coexistence of pro-cyclical and risk-off forces.

- Investors are preparing for a wider distribution of economic outcomes by adopting a more active approach to currency risk management, particularly where gains from prior dollar strength can be crystallised.

- Those with greater flexibility are deploying custom multi-currency baskets to reduce concentration risk and more precisely calibrate exposure to specific economic risks.

- There is a growing recognition that currency volatility itself presents an opportunity set, with dynamic, active allocations across a broader currency universe offering the potential to generate positive return drift over time.

Author

Appendix: Supplementary Charts