Market Commentary – May 2026

23/06/2026

Key Themes Driving Currency Markets

Threat Assessment

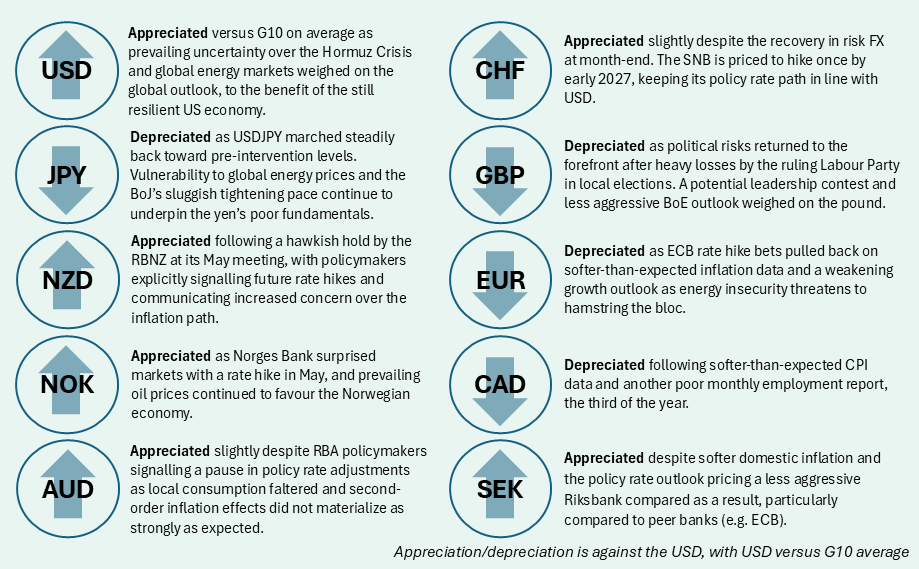

The USD regained traction in May amid a backdrop of rising US Treasury yields, resilient US equity markets and a diplomatic stalemate between the US and Iran. More broadly, FX markets continued to be shaped by shifting geopolitical developments and their transmission into rates, energy and risk sentiment. Fluctuating US-Iran negotiations drove alternating bouts of safe haven demand and risk optimism, influencing near-term USD direction. Investors were increasingly forced to reckon with the material effects of the Strait closure as energy inflation drove hotter CPI readings across markets and a growing number of governments issued energy conservation ordinances.

Month end brought reports of a 60-day memorandum between the US and Iran to extend the ceasefire and open the Strait of Hormuz fully, providing investors with what felt like tangible progress in negotiations after weeks of false starts. Risk FX rallied, further bolstered by a weaker Q1 US GDP report, faltering corporate profits and softer-than-expected PCE inflation. That said, USD rebounded in the opening days of June after Iranian leadership suspended talks over the ongoing Israeli invasion of Lebanon, leading to a renewal of hostilities in the Gulf theatre.

Central Banks Shore Up

At the same time, policy dynamics remain in focus, from FX intervention in Japan to resilient US macro data pushing the FOMC away from its currently held easing bias. Japan’s Ministry of Finance at last intervened against the runaway USDJPY, with multiple rounds of intervention lasting from end-April to mid-May. MoF operations helped push the cross back below the key 160 level; however, in the days following, dollar strength picked back up on Iran War risks, hot US inflation data and hawkish Fed repricing. Indeed, the FOMC’s late-April meeting concluded with multiple members voting to shift the Fed’s policy bias from easing toward neutral. Although no policymakers called for hikes in 2026, market pricing shifted remarkably, moving from a static policy rate to two hikes by end of year.

Energy shock resilience and vulnerability helped to dictate FX movements in Europe as countries hunkered down for a potentially extended closure of the Strait of Hormuz. Swiss held up relatively well compared to the G4 as deteriorating risk sentiment provided a degree of safe haven flows into CHF. However, SNB policymakers warned of excessive franc strength, particularly versus the euro, and drew a line in the sand which investors appeared unwilling to cross, lest they provoke intervention. Sterling suffered as a result of a bubbling political crisis following the ruling Labour party’s wipeout in local elections, prompting a possible leadership challenge against PM Starmer. The BoE kept rates steady as policymakers face increasing inflation pressures and deteriorating growth outlook, leaving few options on the table to address both mandates. ECB policymakers signaled hikes for the summer, in-line with existing market expectations, but the degree of policy tightening remains up in the air as Eurozone growth is weighed down by collateral damage from the Iran War.

N.B.: This summary includes market events and currency movements up to end-of-May.

Please click here for additional information, including risk disclosures.