Market Commentary – March 2026

09/04/2026

Key Themes Driving Currency Markets

Iran War Leaves Energy Markets Languishing

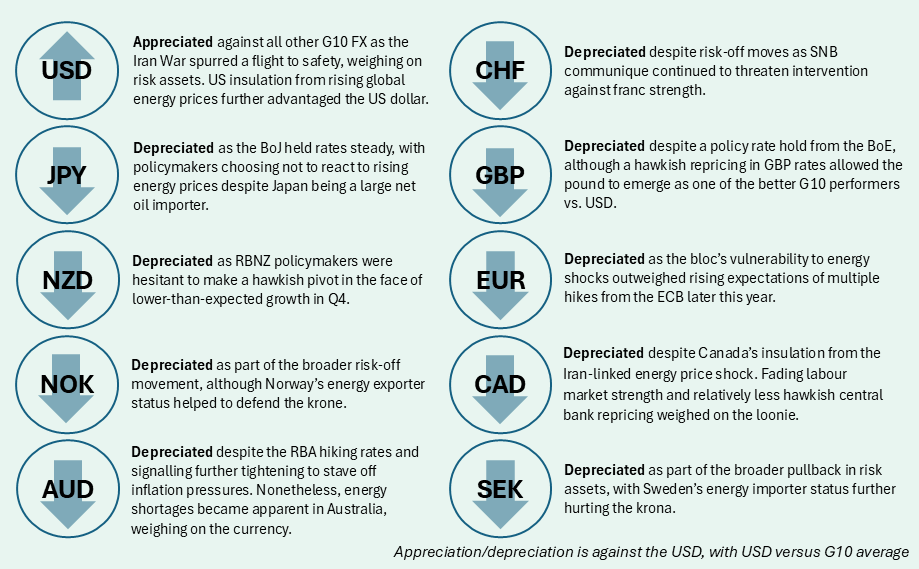

Geopolitics continued to drive FX dynamics this month as US and Israeli strikes on Iran plunged the Persian Gulf into open conflict. Hostilities have led to the effective closure of the Strait of Hormuz and halted oil and gas transfers from the Gulf countries, leading to a spike in global energy prices. On the FX side, safe-haven flows and more favourable terms of trade developments have benefitted USD, with risk FX going largely belly up. In the four weeks since the start of the war, the conflict has shown little sign of letting up, although markets have grasped at any signs of de-escalation, leading to wide intraday valuation swings. Iranian leadership has – at least publicly – shown no intentions of negotiating, and US/Israeli communication has proven nebulous with ever changing goals. The stalemate over the Strait has allowed the global energy shock to become entrenched, and policymakers are now taking seriously the prospects of energy shortages and resulting adverse price pressures.

“Go get your own oil”

The energy crunch was most felt in Asia, due to the region’s high dependence on energy imports from the Middle East. Asian EM economies with the lowest energy buffers, such as Thailand, Vietnam and the Philippines, took extraordinary measures to stretch existing fuel supplies including capping energy usage and withdrawing fuel subsidies. Although major East Asian economies such as Japan, Korea and Taiwan possess larger fuel stores, they remain especially exposed to adverse inflation pressures down the line.

Major petroleum exporters, such as Norway and Canada, were partially shielded from the energy price shock due to their ability to sustain consumption. Certain economies, such as the UK, were relatively more protected due to its lower direct dependence on Middle Eastern imports; the UK imports a majority of its crude oil from the United States and Norway, helping GBP hold ground against the surging US dollar. AUD and NZD were relatively poor performers as the Antipodeans rely heavily on crude imports and possess low stocks of oil reserves.

Central Banks Prep Their Defenses

Surging energy prices prompted dramatic heel turns from monetary policy officials, with a host of central banks communicating hawkish forward guidance during the month. The RBA led off with a well-anticipated policy rate hike, but the vote was closer than expected, somewhat limiting resulting AUD strength. The BoE held pat, with all members voting to hold rates and Governor Bailey hinting at rate increases later in the year. BoE pricing swung dramatically mid-month from two cuts to two hikes priced in by end of year. The rapid change in rate expectations shored up GBP, even as fixed income markets began to price inflation concerns and possible demand destruction.

The ECB kept rates on hold, but expectations mounted for an April hike as policymakers look to defend against looming inflation pressures. SNB policymakers voted for no change and Chair Schlegel stepped up threats of intervention given CHF’s Iran-driven safe-haven appreciation. The BoJ also elected to keep rates steady this month, as expected. Governor Ueda acknowledged energy-driven inflation risks but elected to remain patient on policy rate decisions, with BoJ pricing little changed in the aftermath. JPY retreated vs. USD, driven by Japan’s adverse exposure to energy shocks, and carried the currency close to intervention levels, but strong verbal warnings from the MoF throughout the month kept a lid on yen weakness.

The March FOMC wrapped with no changes to policy, but the new dot plot suggested just one cut is on the horizon in 2026. Powell showed less conviction in his presser, stating that further falls in inflation were needed for rate cuts and that the war in the Middle East makes the outlook for inflation, and therefore rates, uncertain. Swings in central bank pricing dictated a good deal of the larger FX moves seen mid-month, but moves were mainly risk-dominated with the terms of trade influence creeping up as the conflict stretched on.

N.B.: This summary includes market events and currency movements up to end-of-March.

Please click here for additional information, including risk disclosures.