Market Commentary – February 2026

17/03/2026

Key Themes Driving Currency Markets

Takaichi Takes Tokyo

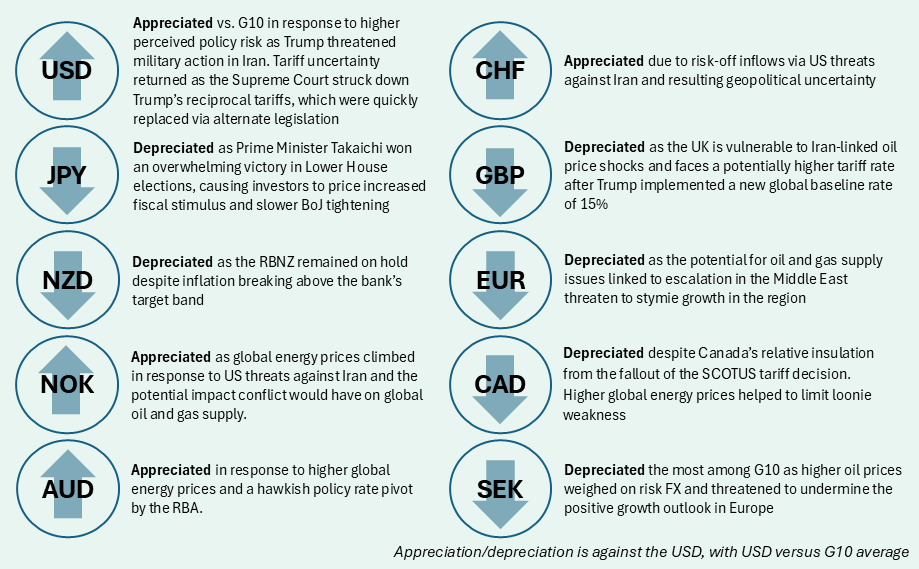

Japan Lower House elections dominated airwaves early in the month with the ruling LDP emerging victorious, overperforming polls and capturing roughly 2/3 of seats. The landslide win provides Prime Minister Sanae Takaichi the mandate she has coveted since taking over a minority government back in October and should afford her the opportunity to pass aggressive fiscal stimulus focused on investment. Japanese equities rallied in the aftermath, and surprisingly so did the yen, defying market expectations. Defensive language from the MoF and pledges to not issue new debt to fund food tax cuts helped to buoy JPY.

That said, the yen fell back to Earth later in the month as Takaichi communicated a preference for lower policy rates and the US renewed pressure on Iran, damaging global risk sentiment. JPY failed to benefit from safe-haven appreciation as Japan is a net-importer of energy and as such would be adversely impacted from an oil price shock. Ultimately, the US and Israel initiated a strategic bombing campaign against Iran on February 28, with Iran retaliating against Israel and US bases in the region. The Strait of Hormuz, through which ~20% of global LNG and oil supply passes through, has been effectively shut down as of this writing. Global oil prices have spiked as there is no clear end to the conflict in sight, raising fears of a prolonged war.

Warfare, Lawfare and Everything In-Between

US dollar weakness in January continued into the following month as incoming data skewed soft and a brief government shutdown delayed key data releases. January hiring data came in higher than expected, but severe reductions to 2025 job growth revealed a nearly frozen labour market that averaged just 15K new jobs per month last year. A leg-down in inflation spurred analysts to push for three cuts in 2026, but hawkish minutes from the FOMC’s January meeting resulted in a quick retreat to two cuts.

After a relatively subdued first half of the month, the US bullied its way back into the driver’s seat as President Trump delivered fresh military threats against Iran, and the subsequent leg-up in global energy prices proved particularly detrimental to risk FX. The surge in dollar strength hit a wall following a disappointing Q4 GDP report and the Supreme Court striking down Trump’s signature reciprocal tariffs. Although the tariffs were quickly re-established under alternative legislation, the defeat potentially weakens the US fiscal position if repayment is required by upcoming lower court rulings. Trump’s negotiating power is also blunted, as counterparties and markets may assume any new tariffs will be struck down later in the year and places existing trade deals in peril.

A Precipitous Position in Europe

Performance was mixed among European FX as the fallout from Iran escalation and SCOTUS decision took shape. Europe’s vulnerability to an energy price shock has become more acute following the EU’s decision to cut off Russian gas imports, and losing access to Middle East supplies could prove extremely challenging for the bloc. NOK initially benefitted from the rally in oil, contrasting with its eastern sibling SEK which dove alongside faltering global sentiment. CHF received some minor safe-haven flows, but the threat of energy insecurity limited franc strength. GBP performance was particularly poor, affected simultaneously by energy concerns and soft employment data resulting in analysts ramping up their bets on a BoE cut in March. Furthermore, calls from within the Labour Party for Prime Minister Kier Starmer to step down present emerging political risks in the UK.

N.B.: This summary includes market events and currency movements up to end-of-February.

Please click here for additional information, including risk disclosures.