Market Commentary – April 2026

14/05/2026

Key Themes Driving Currency Markets

Ebb and Flow

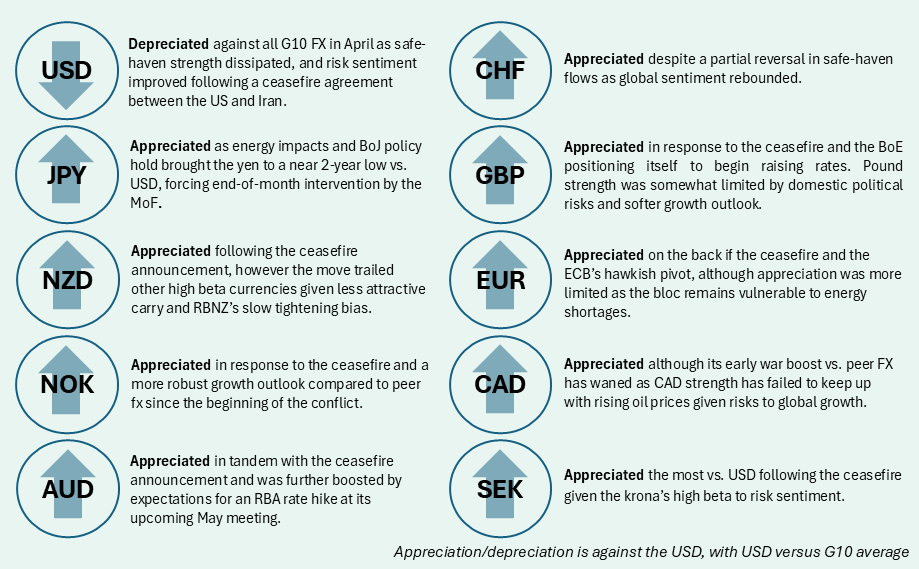

The course of the Iran War continued to shape FX movements in April, marked by a cooling off in offensive operations and beginning of bilateral negotiations between the US and Iran. 7 April saw the start of an uneasy ceasefire between the US and Iran and the announcement of a working agreement to reopen the Strait of Hormuz to shipping. In the ensuing weeks, although hostilities largely ceased between the two parties, negotiations made little progress with the Strait remaining closed and the US establishing a blockade on Iranian shipping. Still, the pullback in hostilities was enough to fuel a recovery in risk assets as market sentiment communicated strong conviction in an inevitable conclusion to the conflict. The ceasefire ultimately helped lead G10 FX higher vs. USD, which weakened to pre-conflict levels on average.

The recovery in risk sentiment was at odds with material conditions on the ground. Benchmark crude moved lower over the month from recent peaks, although prices remained elevated over pre-war levels. Petroleum reserves and a shift toward alternative petroleum suppliers helped to blunt the war’s energy crunch thus far, but shortages became increasingly visible over the month. In addition to rationing measures in Asia, European airlines warned of flight disruptions from May if the supply picture failed to improve.

Central Banks Choose Caution

Rates markets were more reluctant to price in a normalisation of conditions, with central bank pricing still leaning hawkish on balance by month-end. Investors piled on rate hike bets at the start of the war, reasoning that central banks have traditionally tightened policy during oil price shocks and that policymakers would lean hawkish out of fear of another inflation episode so soon after COVID. While communique tilted more hawkish compared to earlier this year, monetary policymakers largely stayed cautious in regard to policy adjustment, with the Fed, ECB, BoE and BoJ all electing to keep rates on hold in April. That said patience is a finite resource, and European policymakers strongly implied they will hike rates over the summer if a higher inflation scenario manifests.

The Fed was less hawkish in its assessment of the policy path; however the April meeting revealed a growing share of the voting body moving toward a neutral policy bias. The FOMC officially still holds an easing bias, but three Fed presidents voted to revoke this stance, hinting at a potential freeze in policy adjustment going forward.

Forcing the MoF’s Hand

The BoJ’s decision to stay on hold proved irksome for the yen, with USDJPY climbing to a near 2-year high over the month. The BoJ’s revised outlook significantly raised its inflation forecasts, implying policy is falling behind the curve in this regard. The yen’s woes ultimately spurred Japan’s Ministry of Finance into action, intervening on the final trading day of the month and issuing further threats of intervention in the days following. The language explicitly highlighted upcoming holidays as a period of thinner liquidity that could be conducive to further market action, likely helping to further boost the yen as investors squared positions ahead of anticipated second-round intervention.

N.B.: This summary includes market events and currency movements up to end-of-April.

Please click here for additional information, including risk disclosures.