AUD: From Tailwind to Headwind? Reassessing Currency Management Approaches

30/04/2026

Executive Summary

Currency management has moved from a background consideration to a key driver of portfolio risk for Australian investors. With the safe-haven status of the US dollar in question and the range of outcomes widening, a “set and forget” hedge ratio could turn yesterday’s tailwind into tomorrow’s drawdown. We argue that now is an opportune time for Australian institutional investors to revisit their assumptions and consider more sophisticated currency management approaches that adapt to market conditions.

The US dollar’s uneasy equilibrium

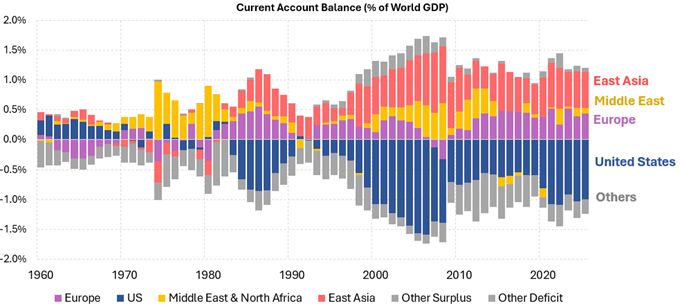

The US dollar is at an uneasy equilibrium. While global imbalances remain deeply entrenched – with the US absorbing the world’s excess savings through persistent trade deficits – its cyclical strength has relied on superior productivity growth and a fiscal-monetary mix that consistently attracts capital flows (Figure 1). Last year’s dollar weakness and elevated institutional uncertainty together suggest this equilibrium is under pressure.

The mercantilist US response to widening twin deficits has, in our view, only compounded these issues. Trump’s tariffs have failed to correct the investment-savings gap in the US, best evidenced by a record Chinese trade surplus last year, as US tax cuts offset tariff revenues. The result has been an acceleration towards a multipolar world order, as middle-powers – led by Europe – reconsider long-standing economic and security arrangements with the US.

The US’s “benevolent” military and financial support of multilateralism has acted as a powerful stabiliser, coinciding with a narrowing in global growth dispersion and a sustained decline in currency volatility over the past five decades. While strategic interdependence between the US and China has prevented the system from outright fracture, we appear to be transitioning towards a more confrontational and mercantilist backdrop; as both countries decouple, the odds of miscalculation and more frequent supply side shocks appear to be rising.

The risk-reward of holding unhedged US dollar exposure is therefore shifting for international investors. The distribution of US dollar outcomes is widening, and there are credible paths to further dollar weakness – including fiscal dominance, an AI-related downturn, or managed currency weakness – alongside scenarios of renewed strength. Furthermore, shifting allegiances and reserve allocation decisions may gradually erode the dollar’s safe-haven status and associated diversification benefits for international buyers of US assets. This state-dependent outlook favours new dynamic approaches that can accommodate both tails.

Figure 1 – Global Current Account Balances (% of World GDP)

Source: G. Nievas, T. Piketty (2025) Unequal Exchange & North-South Relations: Evidence from Global Trade Flows and the World Balance of Payments.

Currency management options for the Australian investor

Investors have long understood the Australian dollar’s tendency to move in tandem with global economic cycles, particularly against the US dollar. For Australian investors’ international allocations, this has provided a natural hedge against fluctuations in foreign markets, informing a preference for low foreign currency hedge ratios; especially in comparison to fixed income holdings where the benefits of reducing currency risk and thus portfolio volatility are more pronounced. Indeed, lower strategic hedge ratios of between 0% and 35% for equity and similar portfolios have proven effective historically at striking the balance between preserving diversification and partially swapping foreign risk-free rates back to (often higher) Australian rates.

Furthermore, lower hedge ratios have facilitated significant foreign currency gains since the global financial crisis. For US equity allocations, the currency component has generated roughly 2% per annum on top of exceptional local US equity returns. That tailwind may now be fading and the US dollar screens as one of the most overvalued currencies globally, with the aforementioned risks cutting against the US dollar’s well-known safe-haven features.

For many investors, a “set and forget” style of currency hedging can remain an appropriate strategic policy stance. Yet those concerned about the dollar’s valuation still have a multi-decade opportunity to crystallise a portion of their unrealised currency gains. The simplest way to implement this is by raising hedge ratios on a tactical basis. However, this introduces new challenges: deciding when to lower hedge ratios again and how to respond if the US dollar strengthens further.

Dynamic Hedging

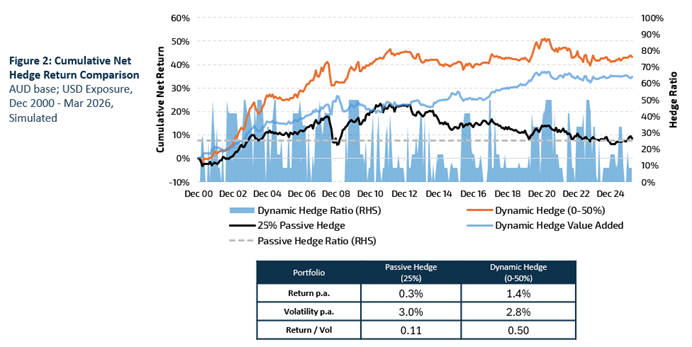

A dynamic approach is a robust alternative, reflecting the possibility of major currency realignments – in either direction – raising hedge ratios in anticipation of Australian dollar strength and lowering them ahead of weakness. Record’s Dynamic Hedging strategy aims to achieve this through a quantitative process which reduces reliance on precise entry and exit timing decisions, and can create an asymmetric outcome profile by changing hedge ratios around an existing strategic benchmark (Figure 2).

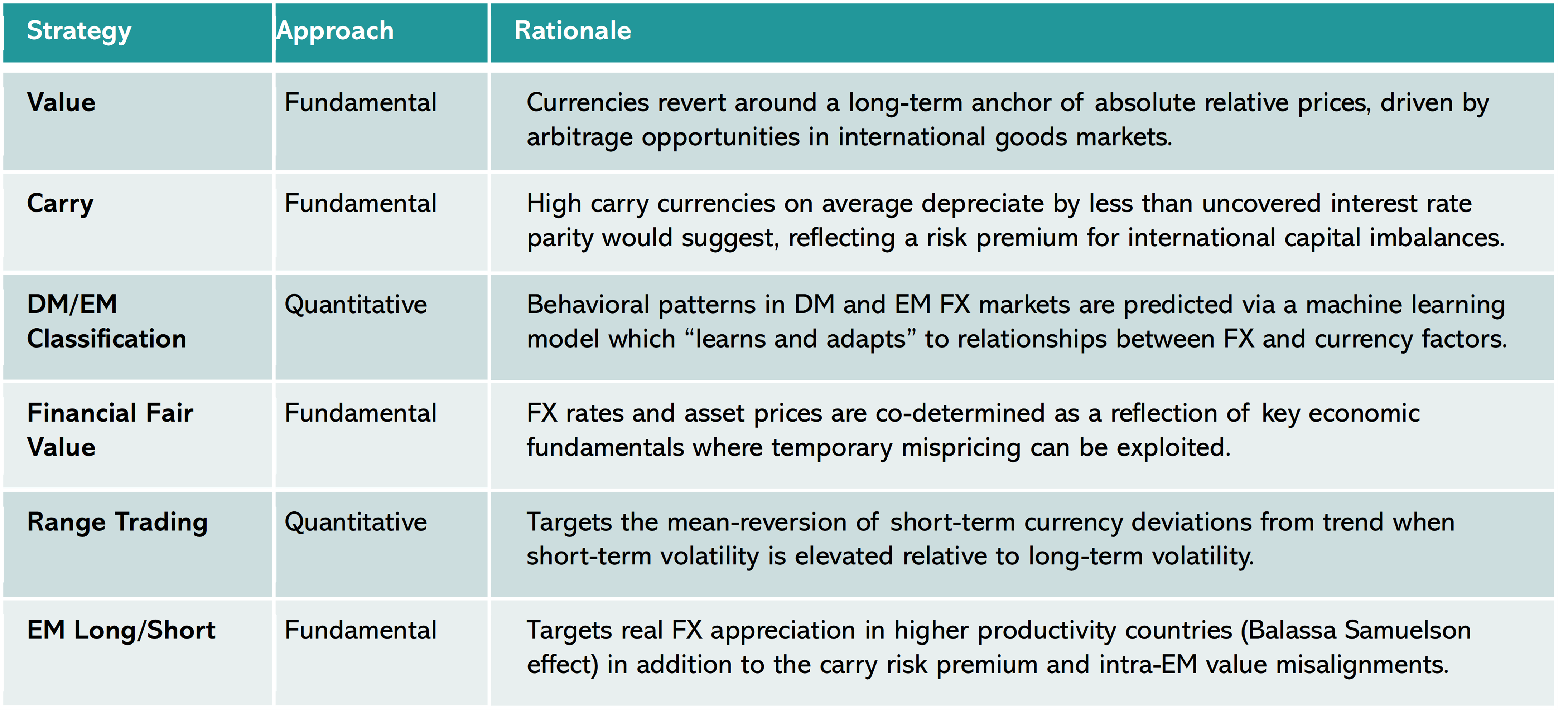

Record’s style of Dynamic Hedging centres around two sets of signals:

- A Factor Allocation component varies hedge ratios in response to market events, trading up to every three days. A machine learning model is used to determine relative importance and directionality of Carry, Volatility, Rates, and US Dollar Cycle factors and anticipate a future exchange rate outturn.

- A Financial Fair Value component adjusts hedge ratios up to monthly when exchange rates become misaligned with their underlying fundamentals as reflected in cross-asset prices (equity performance, interest rates, and commodity prices).

The signals are used to adjust the hedge ratio gradually in a pre-defined hedge ratio range (e.g. 0-50% for a US equity portfolio).

Source: Record, WM/Reuters. Simulation provided for illustrative purposes only. Hedge returns are based on a 1m bullet structure.

Note: Past performance is not a guide to the future. There is no guarantee that any strategy or technique will lead to superior performance. The nature of hedging with derivatives means that there will be intermittent cash flows, which can be large monetary amounts both positive and negative. The use of derivatives means there is credit risk associated.

FX Alpha Overlay

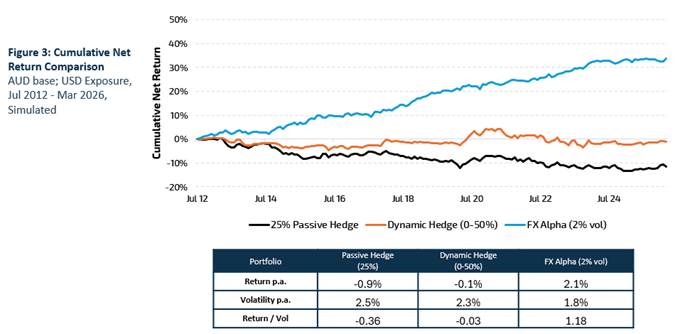

An alternative approach is to treat foreign currency exposure as incidental and inherited through the governance of other core asset classes. Unlike hedging which relies on a stronger Australian dollar to generate returns, an unconstrained “FX Alpha” approach can generate returns across a wider spectrum of economic outcomes. Record’s FX Alpha strategy targets inefficiencies and risk premia in currency markets by investing systematically across a diverse mix of investment styles and time horizons.

Given the strategy’s predominantly unfunded nature its performance can be overlaid on local asset exposures of any kind and with any degree of FX hedging in place, thus enhancing returns across different market cycles in line with the desired risk budget (Figure 3).

Table 1: FX Alpha component parts

Source: Record, WM/Reuters. Simulation provided for illustrative purposes only. Hedge returns are based on a 1m bullet structure.

Note: There is no guarantee that any strategy or technique will lead to superior performance. Past performance is not a guide to the future. The use of derivatives means there is credit risk associated.

Which approach is suitable?

For investors principally concerned about a weaker US dollar, a Dynamic Hedge provides the necessary flexibility to raise hedge ratios within an agreed range, while outsourcing entry and exit timing risks via a quantitative model. Much like a passive hedge, this approach can only generate positive performance in the event of US dollar weakness (give or take the impact of carry). However, the ability to lower hedge ratios can limit hedging losses and provide an asymmetric payoff profile. Furthermore, if centered around a strategic hedge ratio benchmark (e.g. a fixed 25% hedge ratio), Dynamic Hedging can generate value added in environments of both Australian dollar strength and weakness.

If on the other hand, for investors more interested in exploiting a wide range of macroeconomic environments, an FX Alpha approach can be more appropriate given it can trade a wider universe of currencies and features a more diverse set of signals. With that said, it can also help to build a return buffer during periods of Australian dollar weakness – when FX passive hedges underperform – or when the Australian dollar is strong in FX unhedged portfolios.

Return and risk impact

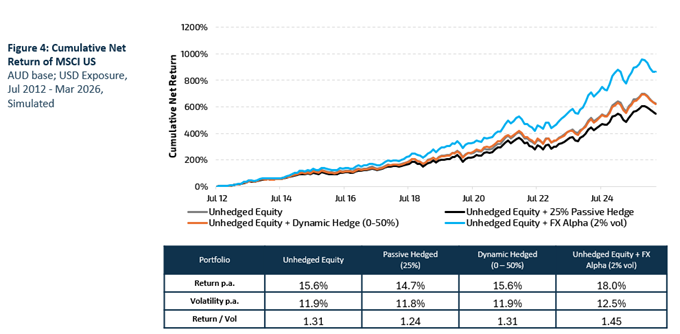

In combination with equities – using MSCI US as an example – a Dynamic Hedge will typically leave portfolio volatility unaffected while targeting a return of 1% p.a. after fees, over a full currency cycle. Whereas an FX Alpha approach targeting a standalone 2% annualised volatility can be expected to raise portfolio volatility marginally (by around 50 basis points) while generating an additional return of up to 2% p.a. after fees (Figure 4).

Source: Record, WM/Reuters, Bloomberg®. Simulation provided for illustrative purposes only. Hedge returns are based on a 1m bullet structure

Note: There is no guarantee that any strategy or technique will lead to superior performance. Past performance is not a guide to the future. The use of derivatives means there is credit risk associated.

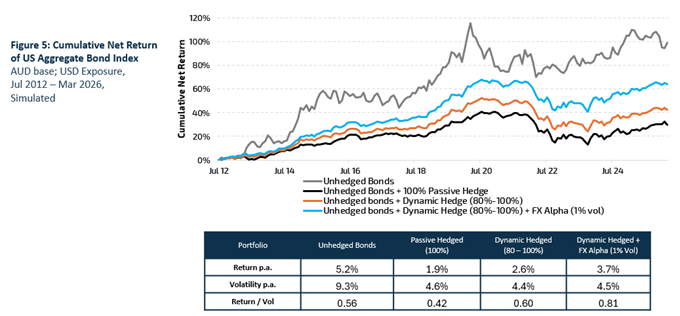

For lower volatility assets like fixed income, maintaining a higher hedge ratio remains the optimal choice given the outsized impact of unhedged currency on portfolio volatility. However, investors can still add incremental value via Dynamic Hedging by allowing smaller reductions in hedge ratios within a range (e.g. between 80-100%).

Furthermore, and similar to equity portfolios Dynamic Hedging and FX Alpha can also be complementary Due to low correlations with local bonds, combining FX Alpha (e.g. with a lower target volatility of 1% p.a.) with a constrained Dynamic Hedging process can generate an additional return of around 2% p.a. after fees, without increasing volatility relative to a fully hedged portfolio (Figure 5).

Source: Record, WM/Reuters, Bloomberg®. Simulation provided for illustrative purposes only. Hedge returns are based on a 1m bullet structure

Note: There is no guarantee that any strategy or technique will lead to superior performance. Past performance is not a guide to the future. The use of derivatives means there is credit risk associated.

Implementation and costs

Both approaches are executed through capital and cost-efficient FX Forwards, the same instruments used in Passive Hedging of FX. The key benefits of both are that they can be scaled to meet specific return or volatility targets, and integrated seamlessly within existing strategic currency frameworks and portfolio asset allocation considerations.

With transaction costs (reflecting FX spreads) in this most liquid financial market forming only a small part of achieved performance, setting up the necessary trading and reporting infrastructure would typically be covered by the services provided by specialist FX managers and thus included into their management / performance fees.

Conclusion

The diversification benefits of low hedge ratios have served Australian investors well, but with major economic and geopolitical change underway, a reassessment is warranted.

For equity investors focused on downside protection, interested to lock in some of the last decade’s accrued gains, Dynamic Hedging provides a systematic approach to adjust hedge ratios within a strategic hedging framework. Those seeking additional uncorrelated returns can use FX Alpha as a scalable solution to enhance performance across cycles and complement existing currency management approaches.

In the case of lower volatility assets such as bonds, hedge ratios should remain high. However, smaller dynamic adjustments to the hedge ratios, in addition to FX Alpha can be a powerful tool for generating additional returns without contributing to portfolio volatility.

Additional Information and Disclosures